Can CBDC Drive Financial Inclusion?

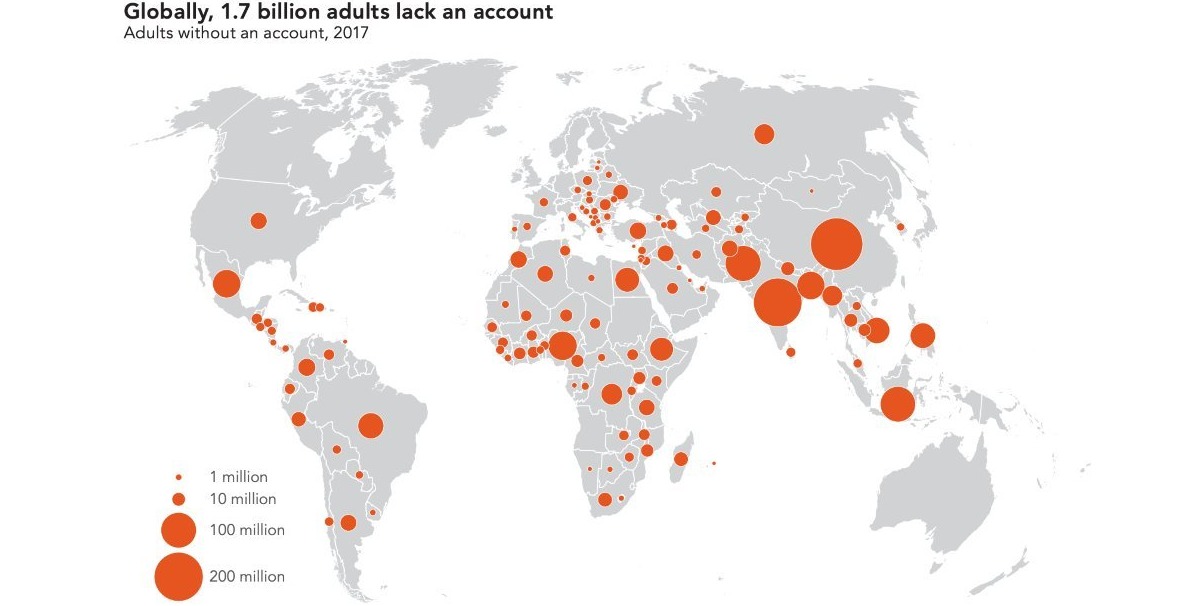

There are still 1.7 billion unbanked in the world. What are the reasons behind such a significant number of unbanked? Can CBDC drive their financial inclusion?

CBDC, or Central Bank Digital Currency, has long garnered the attention of several nations across the globe. Countries such as China, South Korea, Brazil, and Japan are diligently working towards making their sovereign digital currency a reality, taking measures to accelerate its launch. Meanwhile, the Caribbean nation of Bahamas plans to release the Sand Dollar, the digital equivalent of its national currency, by Oct 2020. Contrarily, countries such as Australia do not consider CBDC to be a game-changer.

Yet, many dignitaries such as Tao Zhang, Deputy Managing Director of IMF, consider CBDC to be an efficient payment system that would drive the financial inclusion of those who are today left out of the ecosystem for several reasons. According to Christine Lagarde, the president of the European Central bank, the COVID-19 pandemic has hastened the need for digital alternatives for cash. Even though financial inclusion is higher now compared to a decade earlier, there are still 1.7 billion unbanked in the world. What are the reasons behind such a significant number of unbanked people? Can CBDC lead them towards financial inclusion?

Why are 1.7 billion people left out of the banking system?

The majority of the unbanked population is predominantly found in developing nations. Five south and south-east Asian countries, along with two African nations, account for half of the world’s unbanked population.

Source: Global Findex Database

There are several factors that contribute to people being left out of the financial ecosystem. Very often, the underprivileged populace ends up relying on alternate financial institutions that might exploit these people by charging exorbitant fees for their services.

.

.

Source: Global Findex Database

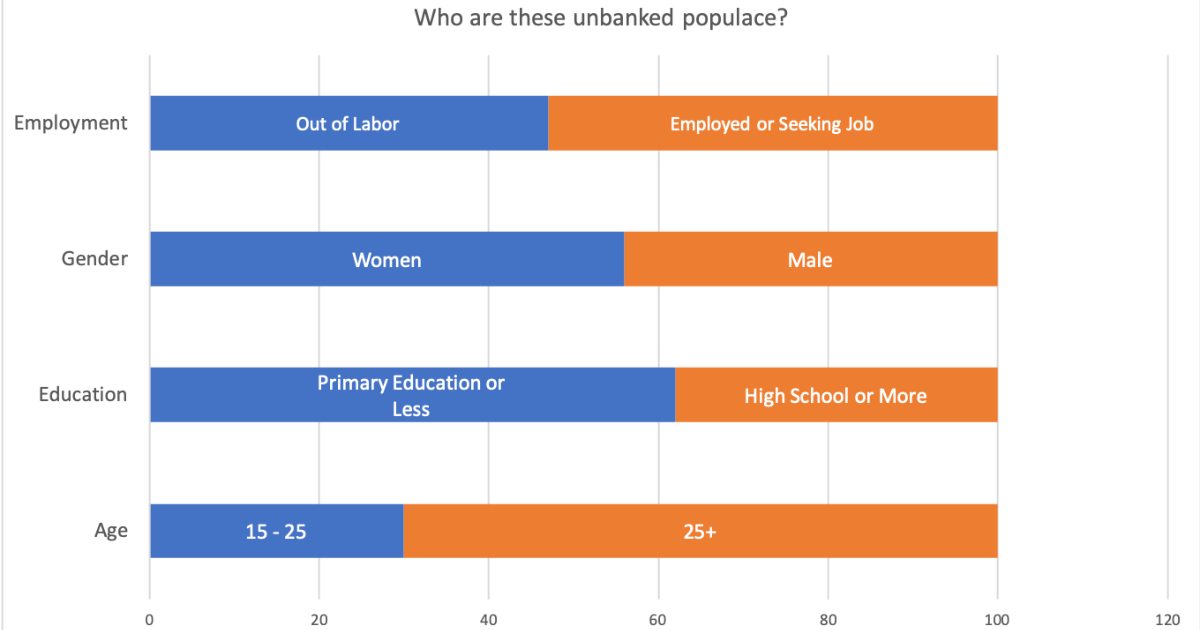

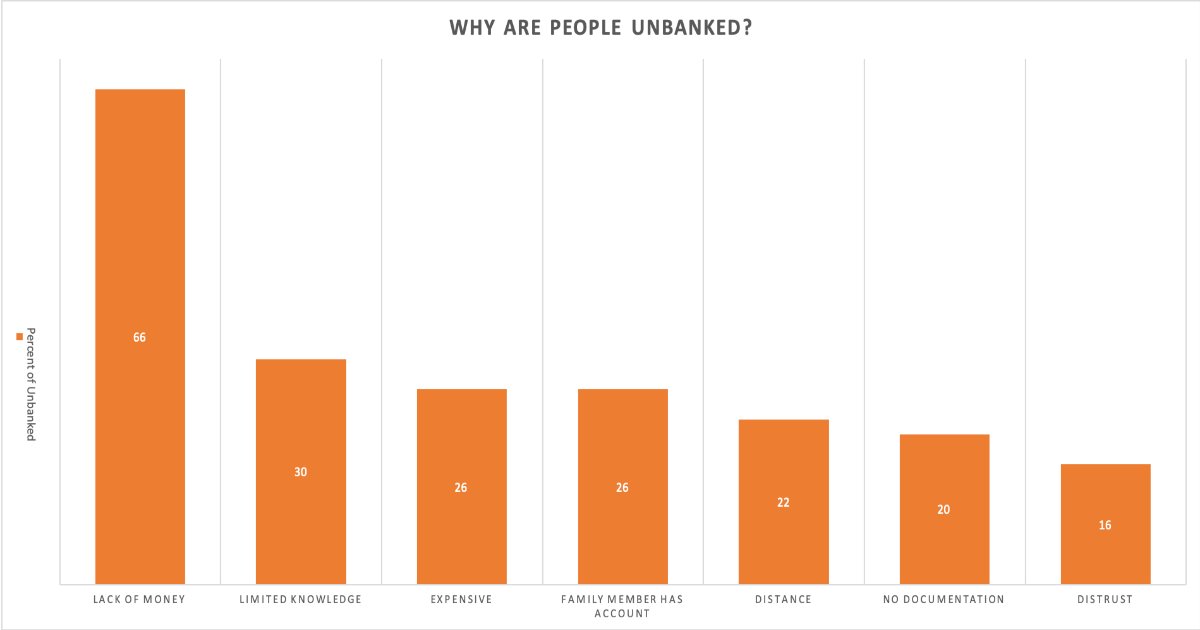

Lack of money is often the reason for not having a bank account

47 percent of the unbanked are out of the labor force. The rest are either employed or seeking employment. Additionally, over 3 billion people globally are either fully or partially out of their workplace due to the COVID-19 pandemic. These people who struggle to make ends meet do not have enough money to open a bank account.

Women are the most unbanked among the unbanked population

Women constitute 56 percent of the total unbanked populace. They often cite another family member having a bank account as the reason for not having one themselves.

Many people have limited knowledge of the significance of financial inclusion

Over 30 percent of those unbanked consider having an account as inconsequential. Additionally, 30 percent of unbanked adults are under 24 years of age. Furthermore, 62 percent of them have primary education or less. So, the lack of financial literacy coupled with indifference towards the financial system has resulted in people being left out of the ecosystem.

Inconvenience to engage with financial institutions is another reason for people shying away from bank accounts

Among the unbanked, 26 percent of the adults consider the cost involved in opening and maintaining the account as a barrier. Besides, for the unbanked populace from the remote places find the distance to travel to their closest bank as a hindrance to open a bank account. Additionally, 20 percent of the unbanked lack the documents that prove their identity and thereby find it hard to open a bank account. Finally, over 16 percent of the unbanked adults do not trust any financial institution.

Can CBDC drive the financial inclusion of the underserved populace?

Cryptocurrencies and Stablecoins are gaining momentum these days. Their usage has been consistently increasing in developing nations of Africa and South America. Daniel Polotsky opines, "Humans are able to transact and send each other money in seconds across the world without an intermediary. If utilized well, this will create a lot more frictionless economic opportunities across the globe, but for this to happen, we must make sure inclusion is prime."

The Central Bank issued digital currency can leverage the private currency framework to foster this inclusion. To begin with, a CBDC has to have universal acceptance. Second, it should be easy-to-use and reduce costs. Third, it should also be interoperable with other payment methods as well as other such digital currencies.

Burgeoning technology can now reach frontiers never tread before

Today, even though there are 1.7 billion people who do not have a bank account, 1 billion among them do have access to mobile phones and moderate internet. Low-price mobile phones have made M-Pesa, a formidable mobile money service in Africa. Likewise, enabling SMS-based hassle-free CBDC transfers will make it easier for people with lower literacy levels and those who are not technologically adept, adapt to digital payments. Similarly, if using CBDC is made easy, it would encourage those who were previously indifferent, to use digital payments.

Governments and private firms should encourage digital wages with CBDC

Several firms operating in countries with most unbanked pay their employees and contract workers in cash. Instead, the governments of such countries should encourage and incentivize these firms to pay wages in digital currencies. Such measures will foster the inclusion of financially underprivileged people into the digital payments ecosystem. Additionally, women who earlier were dependent on their family members to hold on to their money due to lack of a bank account can now save and spend at their will using just their mobile phones. Hence, CBDC enables financial independence for the deprived people.

CBDC-driven payments should facilitate physical ID alternatives for users to authenticate transactions

Stringent document demands make the process of opening a bank account cumbersome. Alternate options, such as one-time-passwords, PINs, and biometrics, can be employed while transacting in digital money. It will lead to the inclusion of those who, for various unfortunate reasons, are unable to produce valid paper-based IDs.

Providing the benefits of the cash system will draw attention to CBDC

For many, the privacy that cash transactions provide is a significant reason to use fiat money. But, such privacy also facilitates nefarious activities and money laundering. CBDC is a powerful solution to this problem. People should be allowed to transact anonymously for transactions of lower amounts. On the contrary, when they use CBDC for high-value transactions, they need to produce a valid ID. These measures will appease both privacy advocates and regulatory authorities.

CBDC should foster trust in the financial system

CBDC is issued by the governments. Hence, it enjoys the reliable backing that paper notes have. CBDC is often considered safer and more reliable than their crypto antecedents. Additionally, Blockchain, when used to undergird the digital currency, adds trust and transparency into the system.

CBDC reduces the reliance on banks and other financial institutions. It can be the medium that fosters the financial inclusion of the underserved populace.

Image source: Shutterstock